Forum

Forum Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Activities

Activities

OPRR

OPRR

Exclusive interview with 1inch: How to innovate in the DEX field under the shadow of Uniswap's monopoly?

Interview: Jack, BlockBeats

Editing: Jack, BlockBeats

Compilation: Jaleel, Kaori, BlockBeats

1inch was born in the 2019 hacker marathon and gained recognition in the 2020 DeFi Summer. Led by two young Russians, Sergej Kunz and Anton Bukov, 1inch has steadily climbed to become a leader in the DeFi aggregator field, thanks to its efficient and low-cost trading methods.

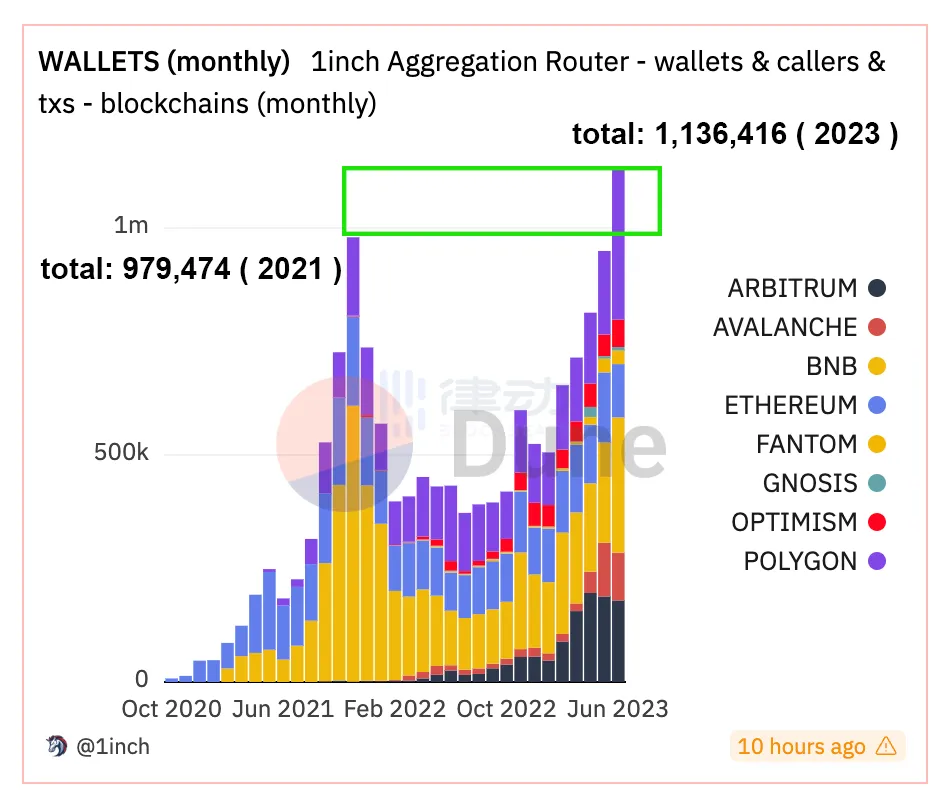

According to data from DUNE, the number of unique wallets using 1inch has exceeded 1 million since last month, surpassing the peak in 2021. Recently, 1INCH has risen above $0.5 and the team has also launched a test version of their developer portal. This Web3 SaaS platform provides APIs for developing new products, including transactions, spot prices, token information, etc.

Correspondingly, another unicorn in the DeFi market has launched a series of attacks. On June 13th this year, the Uniswap team announced the release of the fourth-generation version V4, introducing two new concepts, "Hooks" and "The Singleton". Among them, the former Hooks has attracted particular attention. In the eyes of many, it seems to have become Uniswap's killer to defeat all DEXs. And at the subsequent ETHCC conference, Uniswap launched UniswapX, launching an attack on the liquidity aggregator field. Under such successive attacks, many DeFi entrepreneurs have exclaimed "abandon DEXs and join Hooks".

Last week, during the ETHCC conference in Paris, BlockBeats conducted an exclusive interview with Anton Bukov, co-founder of 1inch, delving into the development history of 1inch, his views and thoughts on DeFi innovation, and how to respond to Uniswap's attack and other topics.

寸拳,1inch 的创新哲学

translates to

One-Inch Punch, the Philosophy of Innovation

in English.

1inch is a name that embodies strong Eastern philosophy, derived from Bruce Lee's famous move "One Inch Punch", which is the translation of the "cun quan" technique in traditional Chinese martial arts.

Before delving into smart contracts, 1inch co-founder Anton Bukov's initial profession was a C++ systems engineer, and then he turned to iOS development because of his love for Apple development tools. However, when he encountered smart contracts, he was immediately drawn to them: when writing smart contracts, one needs to think and write code on a completely new level.

"The importance of accounting innovation has been greatly underestimated"

BlockBeats: 1inch has made a unique contribution in the DeFi field. We have always hoped to have in-depth conversations with the founding team of 1inch, and as far as I know, you are still exploring some new projects.

Anton Bukov: That's right. For example, organizations like =nil; Foundation are working on numerous projects of varying sizes, both within and outside of various large conferences. Some individuals are building new features for existing blockchains and EVMs, while others are dedicated to creating new tools for ZK in the cryptocurrency space. These projects are not limited to existing EVM and Ethereum frameworks, but rather are building future solutions for the mass market of cryptocurrency proofs or protocol-agnostic projects.

For projects that cannot bring any practical value, I am not interested and I do not believe they can bring any practical value. However, there are some people who are doing something. For example, when I talk to them for 15 to 20 minutes, I will find that they are doing something very interesting, they are solving a practical problem. Although this problem may not be very big now, it is becoming more and more important, which is very encouraging.

This specialized hardware can create proofs more efficiently and economically than general-purpose GPUs. They are trying to create a market where you can place an order and if you are willing to pay a certain fee, someone will be interested in your order and complete it for you. Once completed, they will generate the proof and provide it to the smart contract that can verify and pay them.

I once did a similar project at a Hackathon, creating a smart contract that allows users to customize personalized Bitcoin addresses. The contract used a scheme of separated key generation, so no one knows the final private key, not even those who use GPU computing power to search for it. This is impossible. They only know a part of the private key, which is a number that will be added to a number they don't know.

BlockBeats: Is that your first smart contract you wrote?

Anton Bukov: Yes, that was my first smart contract written during a Hackathon in 2017. As I couldn't find any libraries for elliptic curve cryptography in Solidity, it may be one of the most dense and complex smart contracts in terms of cryptography. I needed to generate a private key and public key, add the public key, and then we could calculate the address through the hash of the public key.

I implemented this logic myself, studied how elliptic curves work, wrote the code based on Wikipedia and other documents I found, and it worked. Later, I found a library that provided some kind of intermediate representation in a more efficient way, which was very interesting to me.

BlockBeats: Referring to 2017, many people were focused on speculative activities such as ICOs.

Anton Bukov: It may have been before ICOs, or maybe a few months after, around mid-2017, when we made some jokes about issuing tokens. 1inch may not be as focused on the number of code lines as other fields or projects, because we believe that the key to ensuring user safety is to simplify the code as much as possible and conduct as many audits as possible within the budget.

If you have a protocol with 5000 lines of code and it has been audited once, it is 100 times more secure than a protocol with only 500 lines of code but has been audited 10 times. This is because an audit cannot guarantee that your protocol is secure. Even with formal verification, security cannot be guaranteed. It can only guarantee that it may be secure when you understand all possible combinations. However, you may overlook certain threats and potential use cases.

The past experience shows that some projects that have undergone formal verification may also be subject to hacker attacks. When someone discovers that they can manipulate the price of LP tokens in the same block, they will invest Ethereum and other assets into the Uniswap V2 pool, which causes the price of LP tokens to rise. However, if you have two positions, one using LP tokens as collateral and the other using LP tokens as debt, while manipulating the price, if one position is very large and the other position is negative, then you can leave with a huge position and abandon the debt position.

Therefore, if you can manipulate the price of assets, even raising the price within the same block, this will bring risks to the capital market. This is something that people are not aware of, and formal verification has not solved this problem. A branch of Aave was hacked because of this issue. Aave closed these smart oracles because they were defenseless against such attacks. This is an example of how formal verification cannot make a project 100% secure.

We believe that every audit will increase your security. The less code you have, the more audits you need, the more secure you are. Of course, as engineers with 15-20 years of software development experience, we also spend a lot of time improving efficiency and GAS efficiency. In terms of smart contracts, the only optimization goal is the size and GAS efficiency of smart contract code. We try to find a balance between these two parameters.

Balance between code simplicity and compactness of functionality

BlockBeats: Actually, in the imagination of many people, the code of DeFi dynamic aggregator must be very complex.

Anton Bukov: We will find a balance between the simplicity and compactness of the code, which does not mean that we have to put everything in one line of code. We only do what is necessary and do it efficiently. When writing code, we often use data structures and algorithms to help deal with complexity and gas costs, but we have found another clever way to propose a new accounting algorithm, which is an underestimated topic in the field of algorithms, namely accounting innovation in algorithms.

A member from Paradigm also mentioned this topic on Twitter, and he also believes that accounting itself is an underestimated field that will bring a lot of innovation to DeFi. For example, in 2020, my colleagues and I created a farm smart contract. The first smart contract with a farm incentive mechanism was developed by my colleagues and me for the Synthetics protocol, which sends incentives weekly through a script.

We joined their Discord and proposed, "You provide incentives for liquidity on Uniswap V2, but those who provide liquidity hold LP tokens. Why don't you create a staking contract for these rewards?" They were surprised that we made this suggestion so soon after joining. I also said that we could write this contract. So we wrote this contract and had it audited by Sigma Prime. This contract may be one of the most replicated smart contracts on Ethereum.

You may remember during DeFi Summer there were many "food tokens", which were mainly based on this smart contract. This is an example of an accounting innovation, because an important part of this smart contract is that people can join and leave "farms", which may have thousands or even millions of users. But how does it work when they join and leave?

"Farm" evenly distributes all funds over a period of time, such as distributing a certain amount of tokens every week, every second, every minute, and every block, but these funds are distributed according to the user's staking ratio. There are only three operations here: deposit, withdrawal, and reward collection. None of these operations involve wallet enumeration, and the complexity of this method is called constant complexity. This means that the gas cost required for these three methods to execute is exactly the same, whether we have one thousand users or one million users.

Anton Bukov: Because we see that there is still a lot of untapped potential in this field. Our innovative ideas in algorithms and accounting are very innovative. Despite having currency markets, AMMs, etc., the accounting aspect of this field is still severely underestimated. Take the cryptocurrency market as an example, its operation is very interesting. People deposit their assets into a pool, which mixes everyone's money, and then you can borrow other assets.

For example, you deposit your Ethereum and borrow Bitcoin. You are actually borrowing money from those who have deposited Bitcoin, not from a specific person. Therefore, this process is not peer-to-peer, but rather a pool-to-pool interaction. This model causes your debt and collateral to increase every second.

But how does it work? For example, if half of the USDC collateral is borrowed, those borrowers need to pay 6% interest per year, and their debt grows by 6% per year, but this number is increasing every second. The liquidity providers, who provide half of the liquidity, pay 6% interest, but they receive an annualized return of 3% because half of the 6% is distributed based on a 100% deposit ratio, as a 3% annualized return, and this number is also calculated every second.

Why is it calculated per second? Because initially when I thought of this as a borrowing and lending concept in a black box, I thought that when you repay, you need to pay extra fees. For example, if you borrow $100, you need to pay $105 when you repay, and this money will be distributed proportionally to everyone. But if you only allocate based on the current people in the pool, there is room for manipulation.

Some people may try to front-run and deposit 99% of the liquidity to receive the $5 reward, then immediately withdraw after you. Therefore, you should distribute the $5 reward to all the people who have ever been in the pool, according to their holding ratio over a period of time. Their contribution is to make your debt and collateral grow every second. So for the manipulator, front-running is meaningless because the distribution has already happened. When someone repays the debt, it does not mean that they will pay a sum of money that will be distributed, as this money has already been distributed. This is a great accounting innovation.

Compound and Aave have different implementation methods. Compound rewards users by continuously increasing the price ratio between Compound assets and underlying assets. This price is adjusted every second based on a formula when the borrowing and lending ratio changes. Aave follows a similar approach, but they maintain a 1:1 price ratio, so your balance will continue to grow. This is a different method that can be converted back and forth.

Anyone can write a token wrapper to make it behave like a Compound token. Its balance will not increase, but its price will. And you can also create a reverse wrapper token that allows the Compound token wrapper to behave like other tokens, one-to-one with the underlying asset, with a constantly increasing balance. I believe someone may have already done this project, such as the X token project, which usually creates wrappers that allow similar functions such as voting, automatic voting, and delegation.

Regarding why we choose to innovate in the DeFi field, I would like to say that we are not only focused on DeFi. We are also very interested in Web3 and are seeking innovation in this area. Typically, we come up with unique technological innovations and ideas, and then try to understand whether we can build a useful and successful product based on these innovations and ideas.

I noticed that some projects first envision a product and then try to implement it. But I believe that 1inch's approach is the opposite. We first propose innovation and then try to understand how to best serve users using this accounting method or algorithm. This is also why most of our products can be well implemented when they land, and it is difficult for anyone to compete with them.

Developer Portal, what is 1inch holding back?

On July 19th, 1inch Labs announced the release of the beta version of its Developer Portal. This is a Web3 cloud SaaS platform that provides the most advanced API for developing new products.

1inch Developer Portal provides SaaS solutions, including Swap API that provides quotes for the amount of cryptocurrency that can be exchanged on a specific blockchain for users, Spot Price API that provides the current spot price of cryptocurrency on supported networks based on available liquidity, Balance API that provides accurate information on cryptocurrency wallet balances and limits, Orderbook API based on the 1inch limit order protocol, NFT API that provides information on all NFTs in user wallets, and many other features.

According to official statements, the verified solutions from the 1inch Developer Portal have been successfully tested in both the 1inch Wallet and 1inch dApp. Projects that have integrated the 1inch API include MetaMask, Trust Wallet, and Ledger. The 1inch Developer Portal offers a 99% uptime service level agreement. The 1inch API provides users with extremely short response times, with the lowest latency in the market. Additionally, the 1inch Swap API can access numerous sources of liquidity on multiple blockchains. The user-friendly interface allows users to access the latest documentation, advanced request statistics, and all major upgrade information related to the 1inch protocol.

How should a team view industry innovation?

BlockBeats: Let's talk about products. What is the difference between 1inch's latest developer portal and the API provided to developers before?

Anton Bukov: Many developers in the Web3 field have participated in or are still participating in Hackathons. I believe that delivering results quickly is crucial in Hackathons. There is a Pareto principle at play here, where 20% of effort can yield 80% of results, which is what we should strive for in Hackathons. However, delivering products to real users requires the remaining 20%, which will require 80% of your effort. This is exactly what our new developer portal (DevPortal) aims to address.

We spent a lot of time building all these services for ourselves, our wallets, and our products. Then, we decided that if we could give other developers access to all these high-quality APIs, they would be able to move their own products forward faster, validate their assumptions about market demand more quickly, and achieve 80% of the functionality with just 20% of the effort.

BlockBeats: What types of applications or implementations can developers build with these APIs?

Anton Bukov: The possibilities are endless, it could be a wallet or it could be dApps. If you plan to create a wallet, then 20% of your effort and 80% of the results you get could be the user interface, which could be a mobile or web application. However, developing the backend to obtain all the tokens in the wallet, their prices, historical changes, and records, all of which are on the chain, is a bigger job. But if someone wants to run a new wallet and verify if people like it, they cannot do so without a backend. Now, they can simply use our API to try it out, which is free for most people.

BlockBeats: What role will the 1inch wallet play in the entire 1inch ecosystem?

Anton Bukov: We firmly believe that our mission is to improve this industry and accelerate the development of singularity. Therefore, we believe that the only way for our company to survive is through innovation. We not only want to survive, but also want to continue to innovate, which is the driving force behind our progress. Of course, we sometimes feel that we are competing with other projects, but this is a good thing, because it is challenging for us. We started with Hackathons, and in 2019 we participated in 15-20 Hackathons. Competition is always beneficial for end users.

In every field of blockchain, there is competition between wallets and aggregators, and competition exists in almost all markets provided by Web3, blockchain, and DeFi technologies. However, the biggest winners of these competitions are usually the users, which is really great. This industry is still young, and there may be significant changes in ten years. But everything we are doing now is beneficial for building this bright future.

We have released these APIs not only for our internal use, but also for everyone to use. We believe this will drive the industry to build more applications. We are not afraid of competition because we believe there is huge potential for growth in this field. Even if we only have 10% or 15% market share in the wallet market, we don't care. We still process more than half of the aggregated transactions and continue to strive to increase our market share.

Of course, we will compete for our share. But overall, we hope to accelerate the development of these markets. Our goal is not to compete in small markets, but to accelerate the development of the entire market. Having more diverse wallets may attract more people to join DeFi, and we hope to see the entire market develop faster than it is now.

Balance between product innovation and market growth

BlockBeats: Can you reveal what is the most profitable feature or product of 1inch now?

Anton Bukov: In fact, we did not generate any revenue from Swap because we currently have sufficient funds and we are not in a hurry to make money. We believe that growth is more important now. If we need more funds, there are many ways to do so. But in 2023, I think we still have a long way to go before we stop growing. The entire industry may grow tenfold in the next 3-5 years, so growth is more important.

Many projects allocate all their revenue and investments towards growth, rather than profitability. Many companies, such as Uber, operate in the same way. Sometimes, these companies may struggle to survive due to high leverage, as they try to spend more money to earn more money and invest more. However, the problem is that when investors see where all this money is going, they will find that it is being invested in growth, not just in the DeFi field, but also in constantly growing and emerging markets. Therefore, the largest companies in the market are highly focused on the growth of the entire market and their own growth within it.

BlockBeats: What do you think will be the next major update for 1inch after Fusion?

Anton Bukov: We are currently exploring potential products to focus on next, and have designed some unreleased products. Initially, we had over 10 ideas and brainstormed them. We sorted through these ideas and narrowed it down to three that sounded particularly good. We will continue this process until we decide which one may best meet the current market and situation needs. So there is no specific decision yet. This is also why we have never publicly released a roadmap.

The market changes very quickly, and in six months the market may be completely different, and we may develop different products. We cannot be completely sure what we will do in the next six months. If we have a long-term roadmap, but we change our minds, many people may feel dissatisfied because they think the original roadmap was good and the new one is not. Our goal is to always exceed expectations, so we do not release a roadmap, and there will always be people who think they know better than you and are dissatisfied.

BlockBeats: When discussing the creation of new products or innovations, it is necessary to consider the issue of product delivery, as the market is rapidly changing, especially in the DeFi field. How have you adjusted the development direction of your product and its market adaptability in practice?

Anton Bukov: We won't spend more than half a year developing a product or the next version of a product. Typically, we need much less time, around two to three months, maybe a little more. Some development work may start with solidity smart contracts, and then during the audit, we will have front-end, back-end, and other work. It usually takes about two to three months, maybe a little longer in some cases. If our product cycle is one year, we will be eliminated by the market. When you release it, no one may use it, and it may become useless.

For example, Uniswap team, as far as I know, they usually take about a year to deliver their products. They said this is Uniswap X, and I believe they have been promoting V3 version even more than a year before. However, they have been researching the AMM field all the time, such as V3 is an AMM innovation, and this market has been quite stable in the past one to two years. But when we are building in different directions and different DeFi fields, we cannot accept this situation.

Uniswap strikes again, how will 1inch respond?

Previously, the founder of Uniswap announced at ETHCC that a new cross-AMM, Dutch auction-based aggregation protocol called UniswapX will be launched soon. The community and market have mixed reviews on this upcoming product. Dan Robinson, a researcher at Paradigm (@danrobinson), highly praised the changes that UniswapX brings to the game rules of decentralized exchanges, MEV, and interoperability on social media, and listed five reasons in detail.

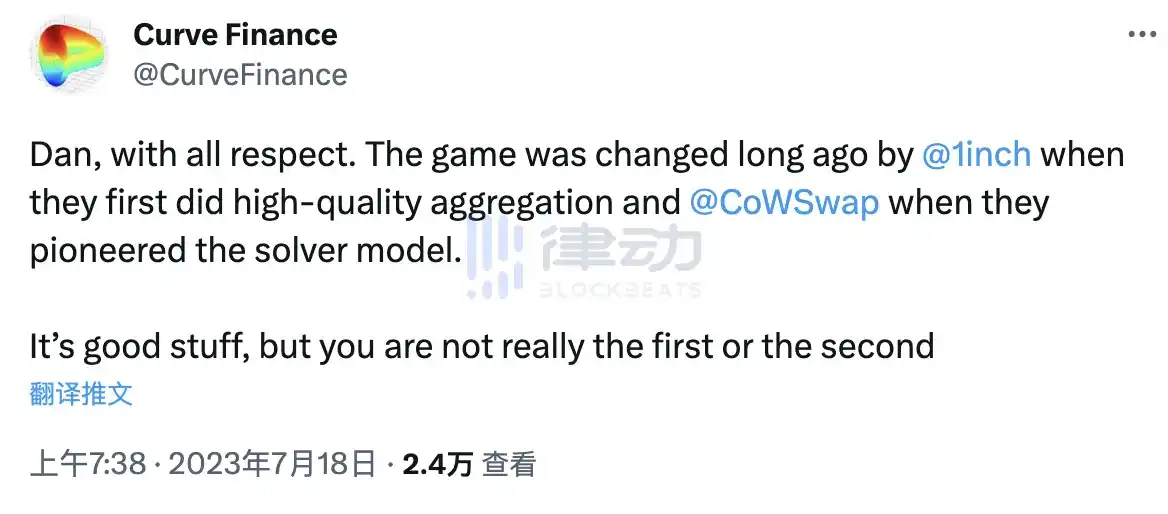

But Curve Finance's official account has a different opinion, and their view has a unique flavor: "Forgive me for being blunt. The rules of the game have changed a long time ago: when 1inch first conducted high-quality aggregation, when CoWSwap launched the Solvers model. UniswapX is good, but it is not the creator, nor even the second player." Undoubtedly, Curve Finance believes that Uniswap is copying. Some community members also questioned: "UniswapX = CoWSwap + 1inch?"

Related reading: "Uniswap: Praised and Criticized, Is It Really the "Tencent of the Crypto Industry"?"

Pink Shadow

BlockBeats: You mentioned Uniswap, which recently released its important V4 version and UniswapX. Although other protocols have proposed similar innovations early on, Uniswap's secondary adoption of these innovations still outshines other protocols. I would like to hear your thoughts on this issue. As a DEX team competing with Uniswap, how should you develop in the DeFi field?

Anton Bukov: When I first heard about UniswapX, my initial reaction was to wonder why it looked so similar to 1inch Fusion. After delving into their whitepaper, we discovered that 1inch Fusion was one of their most important references. I believe this is a positive sign, which once again proves that we and other participants in the market are moving in the right direction. This also emphasizes that we are always one step ahead. I firmly believe that our solution will continue to lead the industry.

BlockBeats: Many different DeFi protocols have made a lot of innovations, but the market has not given them enough attention. But when Uniswap implemented similar innovations, the whole market suddenly felt like a revolution.

Anton Bukov: Yes, I think some projects have an unfair advantage, meaning they have some auditors who, due to brand effects, become their door openers. But this situation is slowly being resolved as the market self-adjusts. People are beginning to realize the existence of aggregators, and when they see DEX aggregators, they almost immediately understand that although DEXs are good, DEX aggregators are always one step ahead. Inequality and unfairness are almost everywhere in the free market and non-strictly regulated market, but this situation is improving. The growth rate of unregulated markets is much faster than that of regulated markets, and their inequality is gradually improving over time.

Anton Bukov: We are not particularly afraid of competition, as most of our smart contract solutions are completely open source. The MIT license allows anyone to use the code we write for anything. We believe that not all software engineers, especially anonymous ones, will respect your license. I have already seen some unknown teams fork before the commercial license for Uniswap V3 expired. A commercial license may prevent some open teams or fair competitors from forking, but it cannot prevent some random public forks.

We believe that it's a good thing if someone is inspired by our ideas. We have developed this product and even if someone copies or modifies it slightly, we are still ahead. When we release a new version, we are usually already working on the next one, and each new version is more advanced than the previous one. So we are not too worried about being copied, we see it as a contribution to the public interest.

Anton Bukov: I believe there is still room for innovation and things to be invented. However, it may not make sense to build a project or product before inventing something significant from a technical standpoint. Simply making minor changes to Uniswap or other projects may not work and will not expand market share. The good thing is that if you can find a good design, XS AMM can get attention because if your protocol can offer better prices compared to other protocols, your protocol will be immediately adopted by aggregators. If it can provide excellent prices and attractive returns to LP, you can succeed.

It is possible that a genius may come up with a brilliant method, release a protocol, and attract around hundreds of thousands of liquidity. This new AMM or DEX may be accepted by aggregators, thus gaining its first batch of trading volume and bringing rich returns to LPs. With more LPs joining, the project will gradually grow and it is possible to occupy tens of thousands of shares in the market.

Before the emergence of aggregators, there were many competitors between newly established DEXs. A participant in a certain Hackathon may come up with a very good solution, which is put into use and gains market share. It used to be impossible to get 10% of the market share, just with an idea and a little liquidity. You had to attract users, because no one would make exchanges, but now, you can automatically gain trading volume.

Therefore, the market positioning of aggregators is different from the current business of Uniswap. After the invention of aggregators, many DEXs appeared. Previously, many DEXs disappeared due to lack of users, but when aggregators appeared, many DEXs were able to survive and succeed, gaining some market share to continue their survival.

BlockBeats: Currently, most people's impression of 1inch is mainly as a DeFi aggregator. How do you plan to define yourselves in the DeFi market in the future?

Anton Bukov: Yes, 1inch's main business is still aggregation, and we don't think the release of Uniswap X will bring about significant changes. We have seen other aggregators in the market, and we have competed with them quite successfully over the past three and a half years. In the first six months, we were almost the only player in the market. I believe things will change, but not as dramatically as some people imagine.

We have some products that are not just aggregators, and we will have more different products. Secondary DeFi may be regulated for different markets, such as secondary DeFi in the United States and Europe, and secondary DeFi for China should also be added because it is a very large market. There may be other markets, such as Japan, which is also a large economy, and we can look at it in terms of the economic scale of countries or country alliances.

BlockBeats: Are you worried that the excessive liquidity of Uniswap in the future will affect the large-scale acquisition and use of 1inch?

From our measurement results one or two years ago, this problem was very serious, but now it is gradually improving. This market, like all other markets, is getting better. Many people trade on Uniswap because they heard about it on TikTok and are not aware of the existence of other DEXs or aggregators, but in any case, they will eventually pay the price for it because this market is just too crazy.

BlockBeats: Some people say they are shifting their strategy to building something on V4 hooks instead of developing new DeFi applications. From your perspective, what is the best strategy?

Anton Bukov: You can introduce some innovations of decentralized trading platforms through V4 hooks, and innovate on top of existing decentralized trading platforms to add additional features such as oracles or similar things. Uniswap has seen their protocol forked many times, but these changes are small and do not actually change the logic of the swap. They are changing other aspects.

This forked V4 will allow other developers to add their own features on top, paid or unpaid, or anything else, without forking their code, and they will still be able to trade through these pools with some hooks, now they won't be trading through SushiSwap or any other platform.

Anton at ETHCC venue

BlockBeats: But will this shrink the market or reduce people's enthusiasm for building their own trading platforms and using aggregators to obtain real-time liquidity, leading to a reduction in the technology stack in the market?

Anton Bukov: The focus of the discussion is not to reduce the number of trading platforms, but to reduce the forks of existing trading platforms. You can have your own Hooks, and we would be happy to charge fees or anything else. But if you want to copy Uniswap without any significant creativity, please do not create forks, as this makes no sense. We may see fewer Uniswap forks, but there may be more Hooks.

BlockBeats: Many developers have given up on plans to create DEX and instead turned to researching Hooks.

Anton Bukov: They can still be implemented to some extent through DEX, but competition has indeed become more difficult compared to Uniswap's V3 and V4 solutions. I believe V4 will be more powerful than V3, and V3 has not completely replaced V2, possibly because V2's GAS fees are much lower, which is why V2 still has a lot of liquidity, and Uniswap and its routers still support V2 and V3. However, it is likely that V3 will be completely migrated to V4, as V4 is better than V3, and retaining liquidity in V3 no longer makes sense. But I believe their routers will support V3.

We have had some ideas about our own oracle and other things, but we always struggle with the need to maintain a brand new AMM and all its liquidity. However, we believe that Uniswap has made great strides in improving this market. Therefore, we are exploring what we can offer, what Hooks we can develop that can significantly improve certain aspects, improve oracles, or increase LP profits. We are exploring all of this and may come up with some combinations that could be successful and attract a lot of liquidity to the Hooks we develop.

BlockBeats: This may be where the aggregator comes into play, and it doesn't necessarily have to be a DEX aggregator, it can be many other things?

Anton Bukov: Yes, there is already an aggregator for profits, DEX, and bridging. I think every market is different, and when we aggregate DEX, we don't increase the user's risk. We can add many DEX from day one, and users won't bear any new risks because our smart contracts handle all the risks. However, when we talk about profit aggregation, this will bring new risks to users, and essentially, it should not be like 1inch. We can hide everything behind a transaction, but I think they should still show users selectivity. Users should decide which bridging to use, which is faster, more than $10, or everything is completed in 2 minutes instead of 20 minutes. You can't make decisions for users.

BlockBeats: I remember you mentioned regulatory issues regarding DeFi at ETH Denver last year, but there have been more and more discussions about regulation recently, such as those related to RWA. Do you still believe that DeFi may need to seek its own solutions on issues such as stablecoins?

Anton Bukov: Regarding regulation, I can say that different countries and regions have different requirements and ideas for regulation. However, the problem is that if they try to regulate by making protocols or users follow rules that are incompatible with non-regulated DeFi, this will not harm DeFi, but will create a sub-market of DeFi, which is a kind of sub-DeFi.

DeFi allows users and a subset of protocols to interact in terms of self-restriction and regulation, so they cannot regulate DeFi and can only create a regulated subset of DeFi in some way. We may see regulated sub-markets for the US and Europe regions, and we already have a fairly large DeFi market. If some countries want their economy to integrate with this emerging industry, they need to accept it.

Regulation is possible, but it should be very weak and should not prevent the acceptance of existing DeFi. For example, we saw a few months ago that Banque de Paris created a stablecoin, which was mocked on Twitter. Its token looks like ERC20, but is completely incompatible with ERC20 and will not be used with most existing protocols in DeFi. You can try to make it work, but it may break things.

Because the existing protocol assumes that ERC20 works according to the description in the standard. If your token operates differently, it may break it. For example, Uniswap V3 cannot run at all because previous versions transferred from the source or smart contract when tracking changes in balances used for exchange or providing liquidity. They would think that the transfer had occurred and the balance had been updated, but in fact it had not, so strange things might happen, and their tokens cannot access existing DeFi. They are creating a new market, and I am curious whether at least one protocol will support their solution. It is unlikely that this will happen, and they will not succeed.

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia