Forum

Forum OPRR

OPRR Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Data

Data

Is the RWA ecosystem an opportunity for Hong Kong’s transformation?

Summarized by AI

Summarized by AI

When discussing the topic of Hong Kong RWA, we first establish two common premises: firstly, Hong Kong RWA refers to compliant virtual asset products on moderately regulated and licensed exchanges, therefore views such as de-regulation, permissionless, and purely digital native blockchain are not within the scope of discussion, but not opposed; secondly, RWA is moving in the direction of both crypto and traditional finance, with crypto seeking to attract larger funds and institutions, and institutional funds seeking to break through and find greater digital financial opportunities, therefore RWA is more about discussing assets that are large enough in scale, whether they are financial assets or physical assets, but it does not deny, for example, the tokenization of a certain item is also a broad definition of RWA.

Concept Origin

Conceptual Retrospect

The concept of RWA (Real World Assets) refers to assets in the physical world from a traditional financial perspective, including physical assets (RA) and financial assets (FA). From this perspective, RWA emphasizes the support of physical assets, even for financial assets, which is different from the self-circulation of virtual assets before defi.

RA physical assets have a wide range, including not only precious metals, real estate, and commodities, but also enterprise equity and private equity, which belong to the scope of RA physical assets. On the other hand, FA financial assets mostly refer to entity-supported financial products or financial derivatives, such as bonds, ABS, REITs, foreign exchange, bills, and gold (futures), etc. In fact, physical assets are often non-standard products, so they are mostly institutional markets. Only a few of them are derived into standard financial products, such as futures or ETFs, which are open to retail investors. Financial assets are mainly traded in institutional markets or interbank markets, and the secondary market is partially open to retail investors. This type of financial asset often includes issuance, underwriting, primary market, and secondary market models.

Asset Category

From the perspective of physical world assets, RWA asset categories can be referenced using the 2020 global currency and market data as a reference (in USD):

-Silver: 43.9 billion

-Gold: 10.9 trillion

-Stocks: 89.5 trillion yuan.

-Global debt: 253 trillion.

-Real estate: 280.6 trillion yuan.

-Derivatives: 558.5 (low point) to 1000 trillion (high point)

From the perspective of traditional asset market data, although commodities/precious metals are high-quality assets, their scale is not the largest. Bonds are very mainstream and large-scale physical world assets, while real estate, although currently experiencing a stable or declining trend, is still a large-scale category of physical world assets. The largest in scale are financial derivative assets.

Due to the scale and valuation methods, there are still some emerging assets that represent the future, such as AI computing power, ESG new energy green electricity, etc., missing from this market data. It is believed that more emerging assets will appear in this market data in the near future. Currently, the scale of the Bitcoin or cryptocurrency market is still in its growth stage compared to the scale of these traditional physical world assets.

Regarding asset investment, an American investment bank has conducted an asset ranking for reference purposes. The top-ranked asset is US Treasury bonds, followed by US technology stocks, US REITs, and Chinese assets, respectively.

New and Old Finance

RWA is the integration of virtual assets and traditional financial systems, which is actually a positive development and trend for virtual assets. This means that cryptocurrency assets are beginning to integrate or combine with traditional financial channels, and existing financial assets are being brought into the digital native world through tokenization. For institutional clients and practitioners in the traditional financial system, they may not consider distributed ledger technology and tokenized RWA assets as cryptocurrencies. RWA tokens can be explained as tokenized shares or certificates on a distributed ledger similar to existing financial assets, which can reduce their panic or resistance.

The new regulations for Web3 in Hong Kong initially focused on security token offerings (STOs), requiring licensed exchanges to trade one or more STOs. Later, more emphasis was placed on security token offerings backed by real-world assets (RWAs), coinciding with the rise of the RWA concept in DeFi. Eventually, Hong Kong Web3 replaced (or upgraded?) STOs with RWAs. However, in terms of compliance with the Hong Kong government and regulations, RWAs are essentially equivalent to STO security tokens.

Background Analysis

Background of Short Money

The background of RWA may be related to the bear market of digital currency. The NFT hot spot in 2021 has also become a fleeting trend in 2022. RWA has become a relay baton to stimulate the digital currency market. However, if we look at the entire digital currency market, it has ups and downs. Under the consensus of a small range, digital currency is growing vigorously, but it also faces various complex problems.

FTX and Silicon Valley Bank are one of the key nodes in the industry. Originally, a large amount of new money was flowing into the cryptocurrency market, but due to the collapse of FTX and Silicon Valley Bank, which caused the overvaluation of new money and high-tech equity by tens or even hundreds of times, the market was suddenly harvested and there was no new money and leverage coming in.

What is the old money doing? In the past year or two, it has been all about the Federal Reserve, continuous interest rate hikes and inflation. The high-tech and high-leverage have already collapsed and harvested. Old money only pursues short-term capital interest rates, and cash is king. As you can see, the US 10-year Treasury bond yield was 3.9% and the 1-year Treasury bond yield was 5.4% a while ago. This means that old money is no longer optimistic about long-term comprehensive returns, but mainly focuses on current cash interest rates. All funds are looking for cash cow assets, which is why the global RWA concept is so popular. Because old money can understand and be familiar with RWA assets, and RWA assets often have operating cash flow.

From the perspective of cash flow, in 2023, the over 90-year-old Buffett flew to Japan to negotiate with several major trading companies, with the core purpose of cash cow assets, which mainly include consumer goods such as food and beverage, commercial retail, tourism and hotels, traditional Chinese medicine, home appliances, consumer building materials, textile and clothing, and home furnishings. These consumer goods stocks have strong profitability, high profit certainty, high operating cash flow, and high dividend payout ratios, and belong to super cash cow stocks.

From the perspective of cash flow, it is also difficult for pure native virtual assets to have native cash flow (operational token income). As a new digital financial market, diversity and inclusiveness are still needed. Especially before there is native operational cash (tokens) flow, it is difficult to have pure native virtual asset financial products, and the equity tokens of pure native Web3 companies do not have a closed-loop ecosystem (it should be noted that if Web3 companies generate FIAT income instead of token cash flow, their equity tokens lack a pure native closed-loop ecosystem).

Therefore, in order to grow into a balanced financial market, diversified and multi-level financial products are needed, which require both native equity STO and RWA that traditional capital can understand. The significance of RWA is twofold: one is to attract old money from established institutions to participate, especially institutional clients; the other is to balance the risk-free or low-risk assets in virtual asset investment portfolio allocation.

Virtual Asset Allocation Background

Currently, whether it's STO or RWA, the key is still PI, especially institutional clients. Retail investors cannot support the market. The key to institutional clients is the growth of Crypto Funds. Currently, there are only 12 licensed (1/9) asset management companies on the uplift list. Only when the scale of virtual asset management expands and there are a large number of funds investing in virtual assets and virtual asset portfolios, can they become institutional clients of licensed exchanges.

Discussing the essence of RWA, especially in conjunction with the two initial premises, is the main topic. It is hoped that everyone can work together to promote genuine RWA products and markets. However, there are always people asking if this is RWA or why it is not considered RWA.

Here, we have compiled a Howey Test for RWA, modeled after the securities industry's Howey Test:

-RWA's earnings and its derivative earnings are the main profits, rather than the incidental earnings of pledging RWA assets as collateral. If the earnings of RWA assets fluctuate and do not affect the earnings of its products, then it is not a true RWA.

3. This investment is a transaction structure for Real World Assets.

-RWA bond or financial product issuance, structural design, pricing, and liquidity trading are included in the product structure, right? If the product structure does not include the trading structure of real-world assets, and the real-world assets are only underlying assets, while the product trading structure is a separate set, then it is not a true RWA.

4. The source of benefits comes from the issuer or third party's efforts.

At the beginning, we talked about a premise: don't get caught up in RWA and digital native assets. Of course, since we are discussing RWA, many innovations often come from within the old world or the edges, rather than a complete game-changer falling from the sky.

Three-layer Structure

Previously, we discussed the main model of RWA, which uses RWA assets as underlying assets and creates digital native tokens such as income tokens or arbitrage protocols in the second layer. Combining token economic models and cross-border integration of asset securitization, we suggest that RWA can be structured into three layers: 1- basic assets, 2- income or arbitrage models, and 3- structured.

RWA, as a security token for real-world assets, is not just a simple process of putting physical assets on the chain and issuing a security token. It involves three levels: from underlying assets, to expected return types, and finally to structured security design.

1) Basic assets are relatively easy to understand, just like US Treasury bonds or real estate. Currently, the popular RWA products in the DeFi industry are basically based on US Treasury bonds as stable basic assets, and tokens or protocols are used for income and arbitrage. At this level, real estate is no longer a good basic asset, why is US Treasury bonds the first? As mentioned earlier, one is stable and the other is cash liquidity. If the Bitcoin spot ETF is approved, the Bitcoin ETF will also become a special RWA basic asset, and digital native tokens will first become real-world asset ETFs and then become RWA basic assets.

2) The profit or arbitrage model combines the cash income or expected income of the underlying assets with the premium arbitrage space, and designs yield tokens or TRS protocols around RWA assets and income. The income tokens or arbitrage protocols can be combined with the income type, cycle, form, layering, leverage, and multiple compounding of RWA assets.

3) Tokenization structure design is a structure that draws on asset securitization and blockchain technology, and realizes smart contracts, SPV, etc. to achieve intelligent contracts and codification of income tokens, smart compound interest, smart arbitrage, etc.

Defi's RWA attempt has given us a good inspiration. We can use RWA as the underlying asset to innovate new tokenized arbitrage protocols and yield tokens. Isn't this a digital native token? Look at those Defi RWA products. RWA assets may not be digital native tokens, but yield tokens derived from the underlying asset chain are digital native tokens, aren't they?

Still struggling with native digital tokens? Think about it again: Is Bitcoin like an RWA that tokenizes energy (electricity) into Bitcoin?

RWA Product Design Pattern Reference

From this three-layer structure, many RWA product models can be deduced. Of course, this also requires different perspectives and different participating institutions to jointly innovate the most suitable RWA product model. In my book "Token Economy Design Patterns", I summarized ten models of industrial tokens: currency, traceability, accumulation, mining, asset, data, content, service, fan, and storage. However, for RWA product design patterns, here are some product design pattern references based on the three-layer structure:

1) Stablecoin collateralized RWA, with RWA assets, especially US Treasury bonds, as underlying assets and interest-bearing assets. Currently, most of the top Defi RWA products are based on this model, with different types of subcategories, such as underlying asset collateralization, Fund, SPV, and so on.

2) Tokenization of asset securitization, based on the yield of RWA assets or expected yield design, can be in the form of Fund type, ABS type, and cash distribution REITs type.

3) RWA Asset-Backed Mode, based on the RWA yield, combined with the lifestyle or consumer IP corresponding to the RWA assets, iteratively designed the Yield farming mining mode.

4) RWA derivatives, designed to address pain points in traditional financial markets, such as reverse repo collateralized financing for bonds, and layered A/B tokens for fixed income.

5) The expected premium of emerging assets is reflected in the current yield and future expectations of emerging assets, using yield bonds or a combination of ST with a portion of expected/governance UT or NFT.

6) Green finance RWA, focusing on carbon reduction and carbon footprint, includes green bonds, carbon assets, and green energy. These are generally designed as fixed-income bonds, but can also be in the form of ST+UT. These are popular targets for European, American, and Middle Eastern funds.

7) Digital Equity RWA, packaging the digital native business with digital equity, is not just equity, but combines the DAO organizational structure of digital native business and income design of digital equity RWA tokenization: "DAO+Stablecoin Cash Flow+Token".

RWA Pain Points Solution

Due to space limitations, we will not delve into it here. The product design patterns will be further explored in future series. RWA must combine physical world assets and traditional financial models, as well as the new world rules of virtual assets and native digital tokens. These cross-border integrations and conflicts also bring challenges to RWA products. When discussing RWA products and how to attract more institutions, we always ask these two questions:

-What is the incremental value of RWA?

-RWA's intrinsic value lies where?

Yes, if there is no incremental value, traditional institutions and corporate clients will not come in; if there is no endogenous value, RWA products will not have differentiation from traditional bond products, especially in terms of expected premium.

We have compiled some pain points and requirements from traditional financial markets that can serve as a reference for RWA product design.

In the new regulations for Web3 in Hong Kong, the 7th virtual asset exchange license is crucial and also the most valuable. However, the trading volume of licensed exchanges must rely on RWA and institutional clients. Why is this so? Firstly, it is difficult for licensed exchanges to achieve large trading volumes with native UT-type digital currencies, especially compared to native trading platforms such as Binance and OKEx. The only opportunity lies in RWA, as the scale of RWA assets is large enough, and traditional financing for enterprise assets such as bonds and ABS starts at 500 million, while REITs start at 1 billion. Secondly, institutional clients are the core support of a trading market, as they have high risk tolerance, relatively mature investment strategies, and investment research capabilities. They can help retail investors eliminate information asymmetry and form pricing capabilities for RWA products based on investment research and pre-sale strategies, while currently, project parties and retail investors are pricing arbitrarily.

交易所需要机构客户

Exchange Requires Institutional Clients

As a practitioner in the encryption industry, I can translate the following Chinese text to English:

"Of course, those who come from cryptocurrency exchanges prefer retail investors the most. Therefore, licensed exchanges in Hong Kong have given up PI and instead applied for retail licenses as soon as possible. However, on the contrary, licensed exchanges need to establish an institutional market ecosystem in order to drive the retail market."

If the exchange is mainly focused on RWA, RWA will need its own digital investment fund, digital securities firm or investment bank, digital trust, including insurance assets (insurance asset management) interested in RWA products, and even overseas funds such as the Middle East, in order to expand the scale. An RWA project can form good liquidity from underwriting and issuance, cornerstone investment, listing on the exchange, to secondary market funds and retail investors. On this basis, there are supporting service providers or derivative institutions, which further expand RWA derivatives such as mortgage loan agreements, interest rate swap agreements, arbitrage agreements, etc., to promote arbitrage and liquidity.

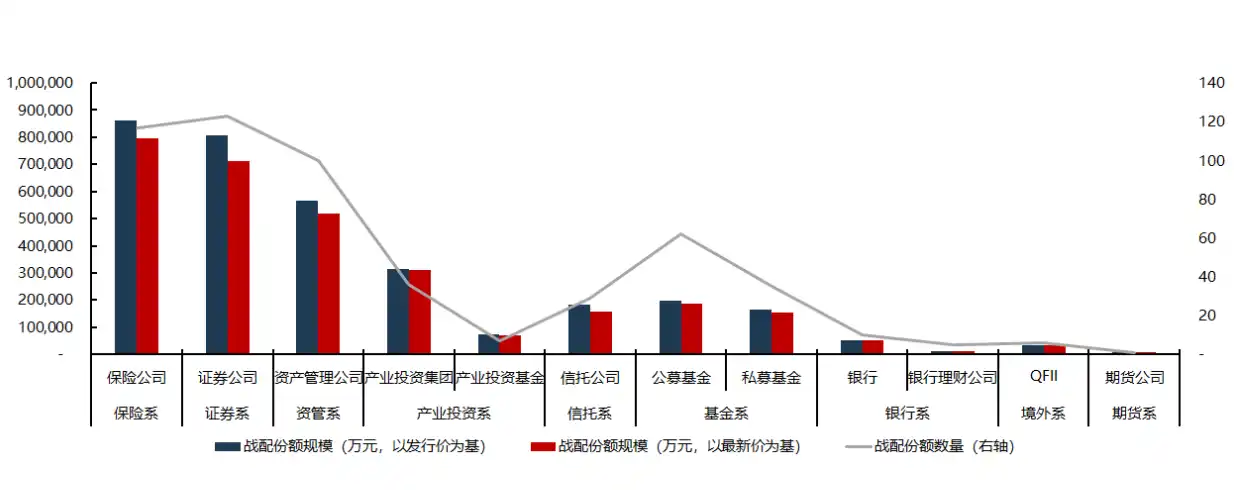

机构客户分布图

translates to

Institutional Customer Distribution Chart

in English.

Around institutional clients, we compared the latest institutional client distribution of infrastructure REITs as a reference for RWA institutional clients. As a mature financing model for enterprises, the institutional clients of REITs are mainly insurance funds, securities, asset management, industry, trusts, funds, banks, and overseas institutions.

(Figure 1 Infrastructure REITS Institutional Client Distribution Map)

However, the primary market for institutional clients may not be suitable for centralized exchanges and may need to go through the primary market before entering the secondary market. Generally, corporate bonds or REITs products are underwritten by underwriters, then cornerstone investors and allocations, or bidding and auctioning, etc., to ensure the issuance scale through the institutional market; then traded in the secondary market. By utilizing the primary market, the product issuance scale can be ensured, and it is also suitable for "pulling down" the ecology of private equity, investment banks, securities firms, etc. Since the institutional market is similar to the interbank market, a centralized trading system is not required. It is possible to consider combining the characteristics of RWA products and blockchain technology to build a business model or trading protocol for a virtual asset inter-institutional market, or the HKEX digital asset sector can consider the RWA primary market, which is of special significance for RWA.

Information Asymmetry and Investment Research Reports

The institutional clients of RWA project can not only solve the problem of financing scale, but also the problem of information asymmetry.

Generally, project parties cannot directly face so many retail investors, even for native digital tokens or NFT projects. They communicate and educate the market through a large number of communities, DAOs, KOLs, and other channels with Hodlers. RWA, as a relatively professional project, especially when it comes to the evaluation, pricing, and structuring of large-scale real-world assets, requires institutional investors' virtual asset investment research capabilities. Institutional investment research reports can serve as a guide for investment strategies and can also truly form the pricing ability of RWA products because currently, both project parties and investors determine pricing arbitrarily.

If it's not easy to understand, you can think about the investment research reports that retail investors often read when trading stocks, aren't they mostly from Sanzhongyi and Huatai Securities? We may not have a clear view of a certain company or industry, but institutional research reports have already analyzed it in detail, avoiding the risk of information asymmetry for retail investors.

Institutional clients provide information empowerment to the retail market through research reports and investment strategies, which may attract support from a large number of retail investors or qualified investors, just like Sanzhong Yihua, and further attract support from a large number of project parties. Such institutional intermediaries have the potential to become giant intermediaries, not only for underwriting but also for secondary trading, and may even become the issuing institutions of Hong Kong Bitcoin ETF or RWA ETF. Of course, for licensed exchanges, this can be a guiding fund for licensed exchanges or an intermediary for a developing digital investment bank.

RWA Derivatives

RWA ecology will also evolve a large number of supporting service providers or derivative institutions. Currently, RWA mainly revolves around a series of products pledged with US Treasury bonds, but it has not analyzed and reconstructed the process and transaction system of corporate financing such as bond issuance or ABS from the perspective of virtual assets. If combined with blockchain technology and some business characteristics of RWA issuance and underwriting transaction models, specific smart contracts or protocols can be designed as an institutional market alternative before the centralized trading retail market, with the cooperation of governance tokens, which is quite meaningful for Web3.

RWA's asset management company (No. 9 brand) or OFC will participate in the primary and secondary markets of RWA products, and may also launch funds that invest in a certain RWA product or investment portfolio in a certain field such as real estate or new energy. It can also provide product services such as regular investment products, intelligent compound interest products, RWA pledge and repurchase, and can also provide quantitative trading for mature RWA products in the secondary market. Therefore, as mentioned earlier, the No. 9 brand asset management company will be a key link in the RWA ecosystem.

Information Disclosure and Investment Orientation

Meanwhile, from a regulatory perspective, the RWA project needs to establish an on-chain information disclosure mechanism as a supplement to the chainlink oracle, which may not necessarily be real-time on-chain, but rather draws on active information disclosure after issuing bonds or listing, to achieve compliance with on-chain information transparency and reflect the compliance and endorsement of licensed exchanges.

In the RWA ecosystem, Maker market makers are indispensable, and they may have evolved from intermediaries. Liquidity in RWA is sometimes "made", and yield is not the core issue. The key lies in product design and trading systems, such as 4.5% yield, fixed-income products with a 3+2 structure, and cash distribution products with quarterly dividends, which all have different liquidity. In addition, with the entry of large intermediaries, institutional clients invest heavily and have access to rich and detailed investment research reports, while individual investors have different investment strategies and liquidity.

RWA products will prompt virtual asset exchanges to consider investment strategy orientation, fairness, and pricing ability. Buffett currently only invests in large consumer cash cow (RWA) assets, which is an investment orientation in itself. This type of institutional client is very valuable to retail investors. As for how to transform it into smart contract products, such as institutional indices or something else, it is a product design issue. As retail investors, we only need to consider risk preferences and suitability; for licensed exchanges, they need to consider these factors because they need to scale up, increase liquidity, and obtain institutional client endorsements.

RWA Digital Investment Bank

The maturity of the RWA ecosystem is demonstrated by the development of RWA digital investment banks. RWA digital investment banks will have strong track (industry) brand management capabilities, and will raise, invest, manage, and withdraw RWA assets through the investment bank model, using digital industry capital (Crypto RWA Fund). They will raise Crypto RWA Fund, invest in and incubate related industry enterprises (assets), issue RWA products, continue to distribute equity and build brands to achieve premium, continue to acquire assets to expand RWA or issue new RWA products, and realize rolling continuous investment exit. In the process of raising and managing RWA assets, they can also design their own token models based on brand IP or asset governance, equity release and other perspectives.

One of the most typical examples in this regard are KeDe and Prologis in traditional industrial investment banks. KeDe has strong brand management capabilities in commercial real estate, while Prologis has strengths in logistics and warehousing. They use the industrial capital investment bank model to achieve fundraising, management, and withdrawal in stages: private equity funds + industrial management and operation + IPO + REITs, forming a capital cycle. For example, KeDe has dozens of private equity funds, corresponding asset packages, and releases some equity/shares to insurance funds, pension funds, etc.; 2 listed companies in Singapore: KeDe Group and KeDe Investment; 6 Singapore REITs. Listed companies and REITs can increase issuance and acquisition, as one of the asset exit channels, or assets can be listed separately. In 2021, after packaging 6 Raffles projects in China, KeDe released some equity to Ping An Insurance to realize a cash inflow of more than 30 billion yuan, and then made a large-scale acquisition of new digital economic assets such as first-tier city data centers.

To sum up, the core of the development of the RWA ecosystem lies in the ability to provide incremental income for asset owners, funders, and institutional clients through virtual assets and smart contracts, which traditional financing lacks. Only in this way can the RWA ecosystem continue to grow and promote its expansion and maturity.

RWA Assets

Traditional Assets

RWA products and ecology cannot bypass their underlying assets. In addition to US Treasury bonds, Hong Kong currently also has real estate, but real estate is actually not the most optimal asset. The investment asset ranking given by US investment banks includes US Treasury bonds, high-tech stock ETFs, North American REITs ETFs, and Chinese assets, which can serve as a reference for RWA basic asset categories.

实际上,从成本和收益角度的老资产已经成为过去时,美债更多是稳定抵押品,不动产投资策略也有了调整,而大宗商品如农产品或者贵金属矿往往是期货或 ETF 指数等金融衍生品,而不是现货资产。以北美不动产 REITs 为例,黑石集团 BlackStone 是最大的 REITs 投资机构,其房地产信托基金 BREIT(Blackstone Real Estate Income Trust)规模为 1250 亿美元,总净回报率为 10.8% 左右。目前黑石不动产最新投资策略进行了调整,其投资组合从逆风向资产(传统的办公室和购物中心)转移到物流、租赁住房、酒店、实验室办公室和数据中心等经营性现金流不动产。

For RWA, real estate may not be as suitable as real estate assets. Real estate asset securitization often involves operating cash flows, such as shopping centers, hotel apartments, industrial real estate, logistics warehousing, and data centers, which are relatively stable assets. The United States is also similar, with large-scale REITs based on real estate, and Blackstone and Blackrock have allocated a large amount of real estate REITs.

New Assets

However, the valuation and financing of traditional assets such as real estate are already very mature and standardized, making it difficult to have opportunities for premium or multiple growth. Opportunities for tenfold or hundredfold growth may not only be those pure Web3 tokens that emerge out of thin air, but those based on real-world assets, especially new assets that advance with human society, such as AI computing power, new energy, new materials, carbon-neutral assets, and so on. Based on emerging assets with clear future expectations and consensus from both old and new generations, new token protocols or securitization products may be the real opportunities for RWA.

These emerging assets, because they are new and inherently digital and online, are relatively easy to switch or upgrade on the chain. Because they are new, existing valuation methods for securitization are not suitable for these new assets: market-based methods cannot be established without a mature market; cost-based methods are disadvantaged compared to traditional assets, especially real estate; and income-based methods have not yet formed stable cash flows. Therefore, it is difficult to have a reasonable valuation of emerging assets using traditional methods, and this is precisely the advantage of RWA security tokens, which can be designed in many ways to anticipate future premiums and expectations.

RWA Asset Category Recommendation

We have compiled a list of asset categories suitable for RWA reference:

2) Bitcoin and Ether spot ETF

3) Operating cash flow of real estate

6) Carbon assets, carbon footprint, and carbon passport.

7) New Space, aerospace and satellite, and Internet of Things for earth, sky, and space.

香港 RWA

translates to

香港 RWA

in English.

Finally, let's briefly discuss Hong Kong RWA. In the future, we hope to engage in detailed discussions and practical cooperation with everyone. In addition to preparing for the RWA Fund and incubating RWA projects through digital investment banks, we will also collaborate with securities firms and banks to launch a financial industry Web3 Guild (DAO) to promote interest in RWA among new and old financial friends. We will organize private board meetings, RWA business discussions, product design, and project cooperation, among other things. If you are interested, you can participate together (WeChat/Twitter: YekaiMeta).

The core significance of Hong Kong lies in its re-export trade and re-export finance, connecting mainland assets and overseas funds. Similarly, for Hong Kong RWA, the core is still mainland RA/FA assets, including mainland institutional clients and funds (especially mainland institutions' Hong Kong branches), as well as overseas funds or assets. Mainland institutions should continue to promote RWA asset investment and financing to overseas funds through Hong Kong's Web3 new channel. In addition to operating real estate or infrastructure, there are also a large number of consumer assets or equities, new energy and new material assets or equities that overseas funds or funds are concerned about. In the case of inability to invest normally, investment and profit withdrawal can be carried out through Hong Kong's compliant exchanges and RWA financial products.

Trading Market Opportunities

The licensed platform in Hong Kong has great opportunities, but it also needs to seize them. Licensed virtual asset exchanges should pay more attention to RWA, and I prefer a licensed exchange platform with RWA as the theme. Only with RWA can it promote the institutional market ecology and underlying infrastructure of virtual assets in Hong Kong, including compliant public chains, stablecoins, and digital Hong Kong dollars; at the same time, RWA will promote broker-dealers, custody, rating, auditing, law firms, and other professional service institutions around RWA assets, and the issuance and underwriting of RWA assets, primary and secondary markets, etc., can also drive the development of more virtual asset management, insurance, trust, and other institutional clients, especially the development of compliance channels for mainland institutional clients.

Against the backdrop of the decoupling between China and the United States and political correctness, it is unlikely for Hong Kong to regain its status as an international financial center through traditional finance. Just compare the daily trading volume and Hang Seng Index of the Hong Kong stock market with the data from 2018 and 2019. The current opportunities may lie in digital finance and green finance. Virtual assets have no borders or political correctness, and every Bitcoin holder is not labeled as pro-American or pro-Chinese. ESG and carbon neutrality are advocated by Europe and supported by the United States, and green finance is politically correct worldwide. It may take time and opportunity for European and American funds to withdraw and return, but some friendly sovereign funds, especially those from wealthy Gulf countries in the Middle East, should focus on Hong Kong's RWA and green finance. In August, we visited relevant institutions and funds in Dubai and fully felt the openness, enthusiasm, and friendliness of Dubai.

Opportunities in Hong Kong Policies and Regulations

Can Hong Kong stay or leave, it depends on the overall ecosystem. The Hong Kong government and regulatory authorities have been very proactive, with the Chief Executive, the Financial Secretary, the Hong Kong Monetary Authority, the Securities and Futures Commission and other relevant high-level officials and institutions frequently speaking out on Web3 and RWA. Relevant legislators have also been active.

From the previous OFC/LPF policy in Hong Kong, to the new Web3 regulations and virtual asset licenses, to the ongoing discussions on stablecoin regulatory frameworks and the digital Hong Kong dollar system, as well as the newly established Temasek investment company and innovation fund in Hong Kong, these are all necessary and compliant measures.

However, what is interesting is that several major families representing Hong Kong's physical industries (especially real estate + manufacturing/trade and transportation) have not yet taken a clear stance or action; at the same time, perhaps due to compliance, Hong Kong has not extensively interacted with mainland financial institutions and engaged in "investment promotion".

At the level of the trading market, licensed virtual asset exchanges are also just beginning. Apart from HashKey's expansion at the end of September, OSL, which obtained its license early on, has yet to expand. Although there are several exchange institutions currently in the process of applying, there are still relatively few companies and licenses for virtual asset management, not exceeding 12.

Meanwhile, the Hong Kong Stock Exchange has been slow to act in the virtual asset sector. The two Hong Kong Bitcoin futures ETFs it previously launched did not make much of a splash, with no oversubscription or much noise. If the Hong Kong Stock Exchange can innovate products such as green carbon ETFs and Bitcoin spot ETFs in the virtual asset sector, it will further promote the landing and development of Hong Kong RWA.

Stablecoins in Hong Kong and RWA

The regulatory framework for stablecoins in Hong Kong will also be a key element of RWA. In the green bond token framework in Hong Kong, we can see a transitional "token" called "cash token" as an intermediary currency between tokens and fiat currencies. RWA is corporate financing, and the current demand for corporate financing is still in fiat currencies. Therefore, market-oriented stablecoins in Hong Kong and the Hong Kong government's digital HKD are crucial for the flow and conversion of RWA funds.

With the Hong Kong stablecoin and digital Cyberport dollar, RWA projects may generate operational cash flow in the form of stablecoins or digital Cyberport dollars, which is very beneficial for structured tokenization. As the scale and stability of RWA assets continue to grow, market-oriented stablecoins may emerge under the regulatory framework of stablecoins, anchored by a basket of high-quality RWA assets (including or combined with Bitcoin and Ethereum ETFs), which can then be called RWA stablecoins.

RWA products will promote the development and growth of the "RWA licensed exchange + RWA project + stablecoin + institutional market" ecosystem. It is important to lay out the RWA market, especially the No. 9 card asset management.

Licensed exchanges are collaborating with the Hong Kong Stock Exchange and relevant institutions to research and launch a Bitcoin spot ETF in Hong Kong, which is also a key opportunity, coinciding with the launch of a Bitcoin spot ETF in North America.

When compared to US Treasury bonds, it may be worthwhile to consider the sovereign debt of countries with advantageous funds, such as the sovereign debt of Gulf countries. Based on RWA, trading on the RWA exchange with sovereign debt collateral or RWA collateral financing, as well as investing in the liquidity market, allows Middle Eastern funds to follow the sovereign debt and engage in circular investment and arbitrage in the RWA exchange and asset pool in Hong Kong.

Throughout history, Hong Kong has been a very unique financial market, not just currently. Some people have left with pessimism, while others are still persistently seeking new paths. From a Western perspective, it seems to have been replaced, but from the perspective of emerging assets, it seems to be reborn.

From the perspective of suitability, there are no financial products that cannot be sold. What's more, virtual assets representing future trends? Compared with the virtual currency of Web3.0, RWA reflects more pragmatism and compromise of Web2.5. We should not easily sing the blues, be fanatical, or be tools for speculators, but actively participate and get involved in the opportunity of virtual asset transformation!

Welcome to join the official BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Official Twitter Account: https://twitter.com/BlockBeatsAsia