Forum

Forum OPRR

OPRR Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Data

Data

Ethereum after re-staking is not what you think

Summarized by AI

Summarized by AI

Original title: "Restaking: Everything Old is New Again"

Original author: David Han

Original translation: Ladyfinger, Blockbeats

Editor's note:

Ethereum's Restaking protocol and LRT are becoming a hot topic in the cryptocurrency field. With the PoS consensus mechanism and becoming the largest security fund in the crypto world with an economic security fund of nearly $112 billion, the concept of re-staking provides a new way to contribute to network security while earning additional rewards. The successful launch of Eigen Layer and the fact that it quickly became the second largest DeFi protocol further demonstrates the potential and appeal of the concept and technology of re-staking.

The re-staking protocol not only provides a channel for validators to earn additional income by allowing validators to re-stake their staked ether to secure new active validation services (AVS), but also brings new security and financial motivation to the entire Ethereum ecosystem. However, as LRT develops and the complexity of the re-staking mechanism increases, new risks have emerged. These risks not only involve security and financial stability, but also include potential impacts on the stability of the future Ethereum consensus protocol.

Foreword

The PoS consensus mechanism is the largest economic security fund in cryptocurrency, totaling nearly $112 billion. But validators who protect the network are not relegated to receiving base rewards only on locked ETH. Liquidity Staking Tokens (LSTs) have long been a way for participants to bring their ETH and consensus layer earnings into the DeFi space - either to trade or re-collateralize in other transactions. Now, the advent of recollateralization has introduced another layer in the form of liquidity re-collateralization tokens.

Ethereum’s relatively mature staking infrastructure and excessive security budget have enabled Eigen Layer to grow into the ecosystem’s second-largest DeFi protocol with $12.4 billion in total value locked (TVL). Eigen Layer enables validators to earn additional rewards by restaking their ETH to earn active validation services (AVS). As a result, middlemen in the form of liquid restaking protocols have also become more common, driving the proliferation of light rails.

That being said, restaking and light rails may pose additional risks compared to existing staking products from a security and financial perspective. These risks may become increasingly opaque as the number of AVS increases and light rails differentiate their operator strategies. Nonetheless, restaking (staking) rewards are laying the foundation for a new class of DeFi protocols. Separate discussions on reducing staking issuance to a minimum viable issuance (MVI) could also further increase the relative importance of long-term heavy yields if such proposals are implemented. As a result, a heightened focus on restaking opportunities is emerging as one of the biggest crypto themes this year. Eigen Layer’s restaking protocol goes live on Ethereum mainnet in June 2023, with AVSs set to launch in the next phase of its multi-phase rollout (2Q24). In effect, the Eigen Layer concept of restaking establishes a way for validators to secure new features in Ethereum, such as data availability layers, rollups, bridges, oracles, cross-chain messaging, etc., potentially earning additional rewards in the process. This represents a new revenue stream for validators in the form of "security as a service". Why has this become such a hot topic?

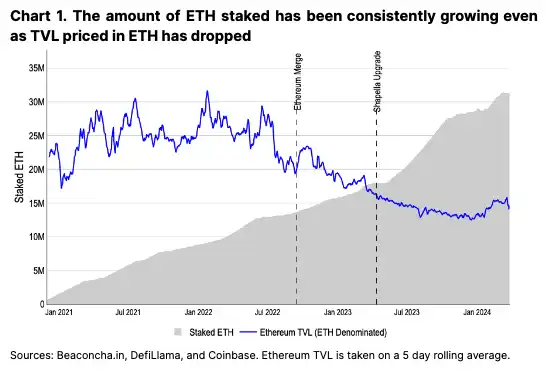

As the largest PoS cryptocurrency, ETH currently has a massive economic foundation for securing its network against hostile majority attacks. However, at the same time, the relentless growth of validators and staked ETH has arguably exceeded what is necessary to secure the network. At the merge (September 15, 2022), 13.7 million ETH was staked, roughly enough to secure the network’s TVL of 22.1 million ETH at the time. As we begin publishing, there are now approximately 31.3 million ETH staked, a threefold increase in ETH-denominated terms, but Ethereum’s TVL in ETH terms is actually lower today (than at the end of 2022) at 14.9 million ETH (see Figure 1).

The excess of staked ETH and the security, liquidity, and reliability of the underlying asset puts it in a unique position to help facilitate the security of other decentralized services. In other words, we believe that restaking as a concept is largely inevitable, as an extension of ETH’s inherent value. However, there is no free lunch. To ensure the correctness of these services, restaking is used for behavioral verification and may be subject to staking or slashing penalties, similar to traditional staking. (That said, slashing will not be enabled when the first set of AVSs are released in 2Q24.) Also, as with staking, restaking operators will receive additional ETH (or AVS tokens) for their services.

Ethereum LRT

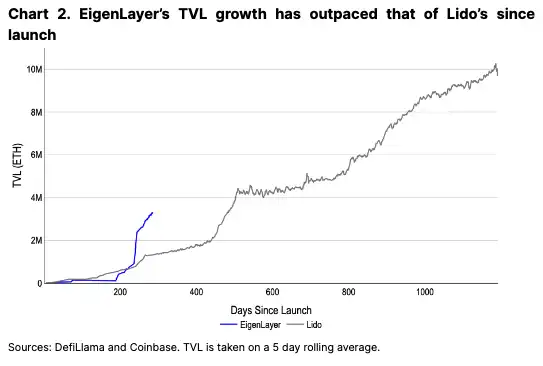

Eigen Layer’s TVL growth to date has been astounding, second only to Lido, Ethereum’s leading liquid staking protocol. Eigen Layer has accomplished this while retaining deposit caps for most of its processes, and before launching any live AVS. That said, it’s hard to decouple the ongoing need for restaking from user interest in short-term spot and airdrop farming. While the amount of re-credited ETH may continue to grow in the long term as the protocol matures, we believe TVL could decline in the short term when point farming ends or if early AVS rewards are lower than expected.

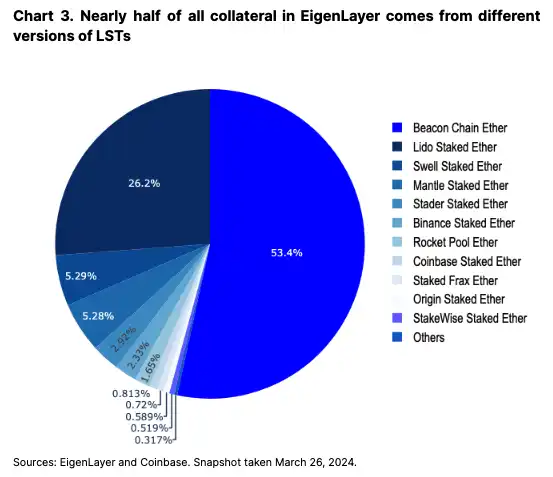

Eigen Layer builds on the existing staking ecosystem by staking diversified base LST or natively staking ETH (via EigenPods). Programmatically, validators point their exit addresses to EigenPods to earn Eigen Points, which are redeemable for protocol rewards in the future. LST locked in Eigen Layer (1.5M ETH) accounts for approximately 15% of all LST, while the overall ETH locked in Eigen Layer accounts for nearly 10% of all ETH used in staking (3M's 31.3M ETH). (LST itself accounts for 43% of all staked ETH in the ecosystem.) In fact, we believe that re-staking is responsible for the recent interest in onboarding new validators after staking demand stabilizes after October 2023. Staking increased by over 2M ETH in February 2024, coinciding with the suspension of the Eigen Layer deposit cap. In fact, some LST providers are increasing their target APY as a way to leverage re-staking interest to attract new users to their own platforms.

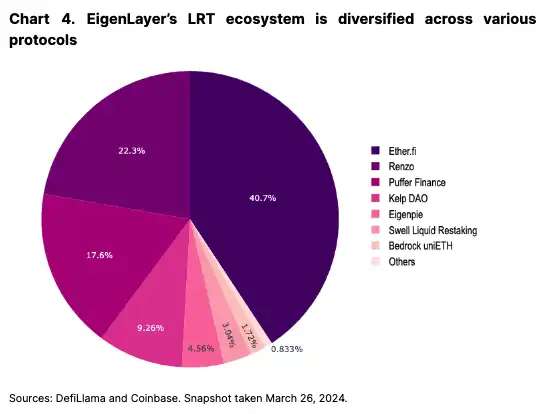

Learning from the popularity of LST, a rich LRT ecosystem has developed with over half a dozen protocols offering versions of liquid reloaded tokens with various points and airdrop schemes. Of the 3M ETH secured in Eigen Layer, approximately 2.1M (62%) is wrapped in secondary protocols. We have seen similar patterns in the liquid staking market before and believe that diversification of alternatives will be important as the industry grows.

In the long term, if native staking issuance declines due to increased staking participation (which reduces yields as more validators join), then restaking may be an increasingly important path to ETH yields. Separate discussions of reducing native staked ETH emission may further increase the relevance of restaking yields (although this is very early in the discussion stage).

That said, AVS yields are expected to be relatively low after launch, which may pose challenges for LRTs in the short term. For example, Ether.fi, the largest LRT, charges a 2% annual platform fee on its TVL for "vault management." However, not all LRTs have the same fee structure, and there is room for competition in this regard. However, if we use this 2% fees as the headline for calculating breakeven costs, AVS would need to pay around $200M in annualized fees ($1.24B on recalculation) for Eigen Layer security services to break even — more than Aave or Maker collected in fees over the past year. This raises the question of how much business AVS would need to generate in order to increase overall yields for ETH stakeholders.

The Emergence of Validation Services

As of today, no AVS has been launched on mainnet. The first AVS to be released (in early 2Q24) will be EigenDA, a data availability layer that can play a similar role to Celestia or Ethereum's blob storage. After the Dencun upgrade successfully reduced L2 fees by more than 90%, we believe EigenDA will become another tool in the modular arsenal for cheaper L2 transactions. However, building or migrating an L2 to utilize EigenDA is a slow process and may take several months to generate meaningful revenue for the protocol.

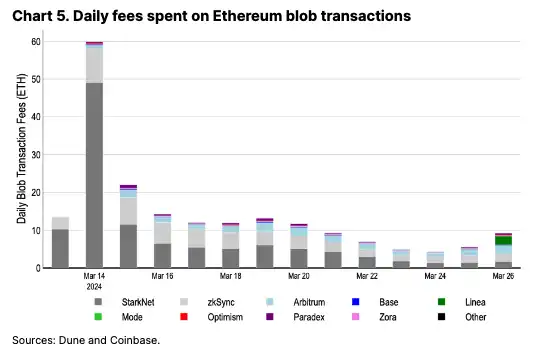

To estimate the initial yield of EigenDA, we can compare to Ethereum blob storage costs. Currently, about 10 ETH per day is used for blob transactions on many major L2s, including Arbitrum, Optimism, Base, zkSync, and StarkNet (see Figure 5). If EigenDA sees similar usage levels, our conservative estimate would be an annualized rate of about 3.5k ETH per year in re-rewards, equivalent to about 0.1% in additional rewards. Fees for the first few months may be even lower than this estimate, although adding multiple AVSs could quickly increase yields.

Other AVSs built in the Eigen Layerecosystem include interoperability networks, fast finality layers, proof of location mechanisms, Cosmos Chain security bootstraps, and more. The opportunity space for AVS is very broad and growing. Restakers can choose which AVS they wish to obtain with their ETH collateral, though this process becomes increasingly complex with each new AVS.

Challenges and Strategies for LRTs

This raises the question of how different LRTs will handle (1) AVS selection, (2) potential slashing, and (3) eventual token financialization. In traditional staking, the one-to-one mapping between validator responsibilities and revenue is clear, making LSTs a relatively simple matter, all things considered. But with restaking, the many-to-one structure adds some non-trivial complexity (and the diversity of LRT issuers) in how gains (and losses) are accumulated and distributed. LRTs pay not only base ETH staking rewards, but also rewards for obtaining a set of AVS. This also means that the potential rewards paid out by different LRT issuers will vary.

Currently, many LRT models have not been fully clarified. However, if there is only one LRT per project, all token holders in a given protocol may be subject to uniform AVS incentives and slashing conditions. The design of these mechanisms may vary from LRT provider to LRT provider.

One suggestion is to take a tiered approach, allowing LRT issuers to adopt a range of "high" and "low" risk AVS, although this requires the establishment of risk criteria that have not yet been defined. In addition, depending on the architectural design, the final rewards of token holders may still be paid out in all AVS, which we believe defeats the purpose of the risk tiered framework. Alternatively, decentralized autonomous organizations (DAOs) could decide which AVS are selected, but this calls into question who are the key decision makers in these DAOs. Otherwise, LRT providers could serve as interfaces to the Eigen Layer and allow users to retain decision-making power over AVS adoption.

Upcoming Risks

However, at launch, the re-staking process should be relatively simple for operators, as EigenDA will be the only AVS that can be secured. However, one feature of the Eigen Layer is that ETH committed to one AVS can then be further spun to other AVS. While this can increase returns, it also increases risk. Submitting the same re-staking ETH to multiple AVSs presents challenges when dismantling the hierarchy of slashing and claiming conditions between services. Each service creates its own custom slashing conditions, so there could be a situation where one AVS slashes the re-staking ETH for misbehavior, while another AVS wishes to reclaim the same re-staking ETH as compensation to the injured participant. This could lead to eventual slashing conflicts, although as mentioned, EigenDA will not have slashing conditions at initial launch.

To complicate this setup further, the Eigen Layer’s “pooled security” model — where AVSs leverage a common pool of staked ETH to secure their services — can be further customized through “attributable security.” That is, it is possible for individual AVSs to earn (additional) re-spent ETH that is used only to secure their specific service — a form of insurance or safety net for paying premiums for the AVS. As a result, as more AVSs are launched, the role of the operator becomes more technically complex and the slashing rules become more difficult to follow. In addition to this re-staking complexity, the scaling of LRTs abstracts away a lot of the underlying strategy and risk from token holders.

This is a problem because, ultimately, we think people will go to where these LRT providers offer the highest rewards. LRTs may therefore be incentivized to maximize yields in order to gain market share, but these may come at the cost of higher (albeit hidden) risk. In other words, we think it’s risk-adjusted rewards, not absolute rewards, that are important, but it can be hard to be transparent about this. This may lead to additional risk as the LRT DAO is incentivized to re-eat at most multiple times in order to remain competitive.

Furthermore, if LRT payments are done entirely in ETH, LRT may also exert downward selling pressure on non-ETH AVS rewards. That is, if LRT needs to convert native AVS tokens into ETH (or equivalent) in order to redistribute rewards to LRT token holders, the accrued value of repurchases may be limited by recurring selling pressure.

Also, LRT has non-negligible valuation risks. For example, if there is an extended staking withdrawal queue (after Ethereum's Dencun Fork, the validator churn limit was reduced from 14 to 8), LRT may be temporarily dislocated from its underlying value. If LRT becomes a widely accepted form of collateral in DeFi (e.g., LST in borrowing and lending protocols), this could inadvertently exacerbate liquidations, particularly in illiquid markets.

This assumes that these DeFi protocols are able to properly assess the value attached to LRT in the first place. In reality, LRT represents a diversified set of portfolio holdings whose risk profiles may change over time. New components may be added or removed, or the AVS themselves may change their yield or solvency risk. Hypothetically, we can see a scenario where a market downturn could affect several AVS simultaneously, destabilizing the LRT and amplifying the risk of forced liquidations and market volatility. Recursive lending would only amplify these losses. On the other hand, protocols that are able to decompose LRT into its principle and yield components could help mitigate this risk, as the tokenized principal could be used as the original collateral and the tokenized yield could be used in interest rate swaps.

Finally, as Ethereum co-founder Vitalik Buterinemphasized, in some cases, a major failure of the refactoring mechanism could threaten Ethereum's basic consensus protocol. If the amount of ETH re-held is large enough relative to all ETH held, there may be economic incentives to execute bad decisions that could destabilize the network.

Conclusion

Eigen Layer’s rebase protocol is expected to become a cornerstone for a variety of new services and middleware on Ethereum, which in turn could provide a meaningful source of ETH rewards for validators in the future. AVS from EigenDA to Lagrange could also greatly enrich the Ethereum ecosystem itself.

That said, adopting LRT wrappers around base protocols could lead to the hidden risks of opaque rebase strategies, or temporary dislocation from the base protocol. It remains an open question how different issuers choose which AVS to issue, and how to allocate risks and rewards to LRT holders. Furthermore, the initial yields on AVS may not meet the extremely high expectations set by the market, although we expect this to change over time as AVS adoption grows. Nonetheless, we believe that rebase supports open innovation on Ethereum and will become a core part of the ecosystem’s infrastructure.

欢迎加入律动 BlockBeats 官方社群:

Telegram 订阅群:https://t.me/theblockbeats

Telegram 交流群:https://t.me/BlockBeats_App

Twitter 官方账号:https://twitter.com/BlockBeatsAsia