Forum

Forum OPRR

OPRR Finance

Finance

Specials

Specials

On-chain Eco

On-chain Eco

Entry

Entry

Podcasts

Podcasts

Data

Data

Decentralized stablecoins issued with ETH as collateral: the key to restoring ETH’s lost value

Summarized by AI

Summarized by AI

Original author: Asher, co-founder of Pure.cash Labs

"The significance of stablecoins issued by ETH has been greatly underestimated."

To this day, many ETH believers, including me, firmly believe that the value of ETH comes mainly from its positioning as a programmable currency, rather than the so-called "ultrasound" narrative.

BTC has successfully completed the narrative transformation from digital cash to digital gold, consolidating its position as the largest cryptocurrency. If ETH adopts the ultrasonic currency narrative and focuses on earnings and valuation, it will severely limit its potential for growth and value appreciation. Under the current landscape, Ethereum's earnings are far less than those of centralized stablecoins and exchanges, and are often even surpassed by application layer protocols. Should ETH's market value be compared with them?

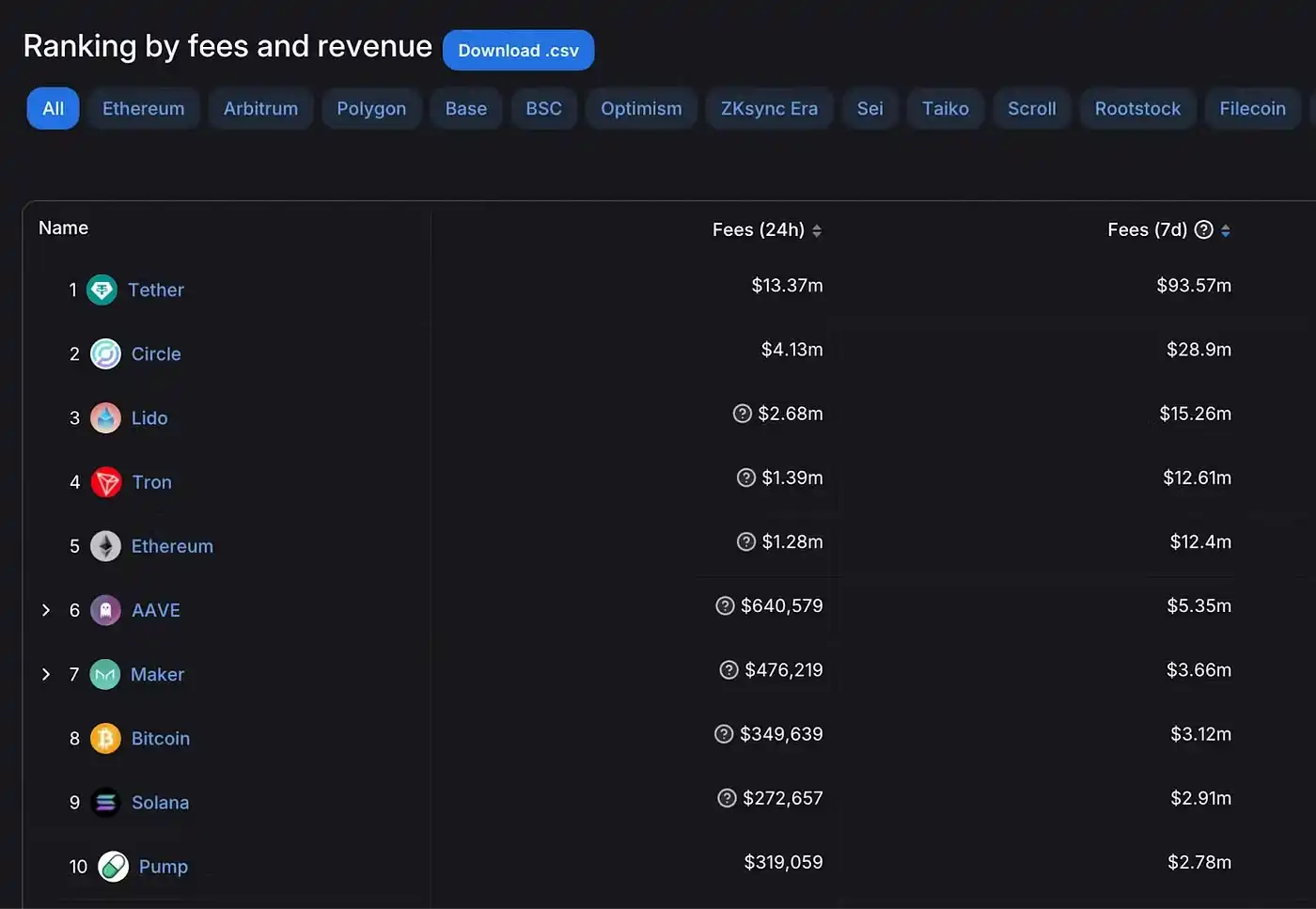

DefiLlama 7-Day Fee Ranking, September 8, 2024

ETH must break away from the ultrasonic currency narrative to keep pace with BTC, or even surpass it in the future. Imagine if BTC abandoned its digital gold positioning and switched to a revenue-based narrative — how much would it be worth? The path forward for ETH is already clear.

Objectively speaking, the peak of ETH as a currency occurred during the ICO boom in 2017. Although the speculative nature of ICOs made this peak unsustainable, it still demonstrated the power of ETH as a "medium of exchange" and "measure of value." However, as the market matures, the current reality is cruel, although many people are reluctant to face it. Putting aside the distant possibility of ETH becoming a "real world currency" that replaces the US dollar, what does the current landscape look like?

· In fact, ETH’s role as programmable money has been largely replaced by USDT and USDC.

· The unfortunate reality is that USDT and USDC are backed by real-world assets, which drives demand for those assets, not ETH.

· Worse, USDT and USDC are centralized, and their issuers have the power to censor and freeze anyone’s tokens. This goes directly against Ethereum’s core values and further undermines the decentralization of its ecosystem.

This essentially deprives ETH of some of its core positioning (remember that the roles of ETH tokens and Ethereum as a network are different), weakens its intrinsic value, while taking advantage of Ethereum's security and permissionless nature for massive expansion and injecting a centralized element. This is a Trojan horse in the Ethereum ecosystem.

But it is not fair to evaluate this situation one-sidedly. In the absence of better alternatives, the rise of USDT and USDC has objectively promoted the development of the crypto industry and demonstrated to people outside the crypto field the possibility of going beyond "token investment": secure, convenient, seamless, and global payments that do not rely on traditional banks. Therefore, from the perspective of market demand and its contribution to the entire industry, centralized stablecoins are not only necessary, but are likely to exist and even dominate for a long time.

Even if most people agree that "centralized stablecoins are not only necessary, but will continue to dominate in the long run", few people will disagree with the view that "decentralized stablecoins are also indispensable". Now I will analyze why decentralized stablecoins, especially those issued by ETH collateralized, are not only necessary, but also crucial, and play an important role in shaping the value and positioning of ETH itself.

Restoring the value of ETH as programmable money

Compared with centralized stablecoins, decentralized stablecoins issued by ETH collateralized inject direct momentum into ETH, forming a positive feedback loop: the more stablecoins are issued, the higher the demand for ETH, which in turn pushes up the price and market value of ETH. As the market value of ETH increases, the potential for stablecoin supply also increases. This effectively converts a portion of ETH into stablecoins and retains the value within ETH itself.

At this point, someone might ask: if the opposite happens, will a negative feedback loop be created, leading to a death spiral similar to LUNA? I want to clarify that this is a completely different situation.

Apart from the flaws of the algorithmic stablecoin mechanism itself, LUNA's stablecoin UST lacks real demand support and relies on Ponzi-style "super-high interest rates" to accumulate value. On the other hand, various stablecoins on Ethereum have been issued on a large scale and widely used in the real world, proving that the demand for stablecoins is real - USDT and USDC do not attract deposits through interest rates, and their supply is driven by market demand.

In other words, Ethereum has built a huge ecosystem with real demand for stablecoins (currently totaling $82 billion). The next step is to explore how to recover some of the demand occupied by centralized stablecoins and return these values to ETH.

Exploration of decentralized stablecoins based on ETH

MakerDAO, the pioneer of decentralized stablecoins on Ethereum, initially relied only on ETH as collateral to issue stablecoin DAI, but soon the limitations of CDP in funding efficiency became apparent, causing MakerDAO to gradually turn to centralization in pursuit of a larger market share. Now even the MakerDAO and DAI brands have been completely abandoned, which is really regrettable.

Currently, the only remaining decentralized stablecoin issued with a certain scale and pledged by ETH is Liquity's LUSD, which, like the original MakerDAO, is based on CDP. However, its supply is only $70 million. Aave, the leading lending protocol, has a total locked value (TVL) of over $10 billion, and its GHO stablecoin, issued by multiple assets, has just exceeded $100 million in issuance due to CDP limitations.

Since the limitations of CDP cannot be overcome, is there a better model? Yes - the Delta neutral hedging model is the key to solving the scalability problem. However, early attempts to apply this model to decentralized stablecoins failed, mainly due to the lack of suitable hedging venues or competitive perpetual contract products. Ethena took an unconventional approach to solve the hedging venue problem by hedging on centralized exchanges, quickly expanding to $3 billion. However, the inherent uncertainty of volatile funding rates and various centralized risks makes it difficult to drive real demand for its stablecoins, mainly attracting short-term arbitrage capital.

Pure.cash, through its "excess demand model", will become the first stablecoin protocol to solve the scalability problem of decentralized stablecoins issued by ETH. For a history of decentralized stablecoins and an analysis of the principles of Pure.cash, see The Path to the Holy Grail: Solving the Impossible Trilemma of Stablecoins.

Pure.cash's Stablecoin Supply Potential

Pure.cash essentially decouples ETH's volatility, while satisfying the dual demands of zero-interest ETH long positions (LongOnly) and stablecoins (PUSD) issued against ETH. These two demands reinforce each other, ultimately increasing demand for ETH. This interaction effectively drives the recovery of ETH's value while re-accumulating the value of programmable money into ETH.

To achieve a "perfect" mutually reinforcing driving force, scale is key. Let's analyze the potential supply size of PUSD.

Currently, the open interest of ETH perpetual contracts is about $10 billion, and combined with leveraged long positions obtained through borrowing, the total long exposure of ETH is estimated to be about $12 billion. The interest cost of perpetual contracts and leveraged loans severely suppresses additional long demand. In particular, the volatility and high cost of perpetual contract funding rates encourage high leverage and short-term positions, severely limiting long-term holding demand.

For example, without considering the cost of funding rate, 1.2x leverage (equivalent to 0.2x coin-based leverage) can increase the return of long-term holding of ETH by 20% with little risk of liquidation. Although this is an excellent strategy to increase the return of holding positions, the cost of funding rate makes this strategy unfeasible. Pure.cash's zero-funding mechanism for long ETH, coupled with a trading fee of only 0.07% (the spot market average rate), is very suitable for the needs of long-term holders and has the potential to unlock more potential demand and convert a large number of spot market users to LongOnly users.

In addition to the above new demand, LongOnly also provides up to 10x leverage while meeting the needs of most existing ETH long traders. We estimate that its open interest may reach $3-5 billion in the short term. As the market potential gradually unfolds, this size may expand to $10-30 billion, supported by the continued growth of the crypto industry, and grow together with the growth of ETH. The size of LongOnly's open interest corresponds to the potential supply of PUSD.

Conclusion

Based on the above analysis, Pure.cash is expected to create tens of billions of dollars of long-term demand for ETH by transferring part of the value of programmable currency back to ETH, becoming a powerful catalyst for the growth of ETH's value.

This article comes from a contribution and does not represent the views of BlockBeats

欢迎加入律动 BlockBeats 官方社群:

Telegram 订阅群:https://t.me/theblockbeats

Telegram 交流群:https://t.me/BlockBeats_App

Twitter 官方账号:https://twitter.com/BlockBeatsAsia